Rebate Calculator ( Move the Slide)

Money saved is money made. if you are receiving $10,000 as your rebate and your annual salary is $100,000. you are simply giving yourself a 10% raise. It is your hard earned money and I am here to help you keep it. Be smart with your money. Contact me NOW

|

|

Simply fill in the Form to tell us what you are looking for, we will contact you how we can help. We believe no pressure sales, after all this is the biggest investment in your life. You need to get all the information and chose who to work with. We would like to earn that trust.

|

Where do I want to live?

It’s helpful to narrow down your search to the key neighborhoods where you want to live. Keep in mind, you may need to expand your search (based on what’s affordable for the area), but it helps to have a starting point. If you have children, check the available school options in your area. What can I afford?

You’ll first need to determine what’s affordable. Keep in mind, when you’re buying a home, you’ll have upfront costs—down payment, closing costs—and you’ll need to be prepared for these expenses. |

What do I want/need?

Make sure you have a good idea of what you’re looking for in a new home and prioritize accordingly. There are many quality and affordable homes—from townhomes and condominiums to single-family or multi-family homes—so make sure you conduct a thorough search. You may not be able to get everything on your wish list, but knowing what your requirements are before you get started will make your search easier. What do I need to start? Before you get serious with your search, you’ll want to find a real estate agent and get your financing in order. We’ll go through these steps in detail, but it’s a good idea to start gathering your financial records (pay stubs, W2s, bank statements, etc.) and have them ready. Have a co-borrower? Their information will be required, too.

|

How much do I need to put down?At one time, lenders may have required a 20% down payment to buy a home. Today, there are options for homebuyers who can’t afford to pay that much upfront. Check with your lender about mortgage programs that allow down payments as low as 3% of the purchase price. One important thing to note, if your down payment is less than 20%, you may need to pay what’s called Mortgage Insurance (MI) each month until you reach 20% equity in the home. Ask your mortgage company about specifics for MI cancellation.

|

Determine your budget Don't look for homes until you know what you can reasonably afford. Remember to not only factor in your monthly mortgage payments, but also taxes, insurance, maintenance and any other monthly costs (car, student loan, credit cards). You can use our Mortgage Calculator to help estimate your monthly mortgage payment.

Find a Lender Now that you have an idea of what you can spend, it’s time to find a lender. Unless you are paying cash for the home, you’ll need to work with a lender to secure financing. And similar to the process of finding a real estate professional, you should talk with a few lenders to find the best fit for your situation. Remember, while the interest rate you’ll pay is a big factor, it shouldn’t be the only factor. Also consider—the different types of loan options available, their customer service, closing costs and other fees, etc. This is the largest financial investment you’ll make, so shop around.

Find a Lender Now that you have an idea of what you can spend, it’s time to find a lender. Unless you are paying cash for the home, you’ll need to work with a lender to secure financing. And similar to the process of finding a real estate professional, you should talk with a few lenders to find the best fit for your situation. Remember, while the interest rate you’ll pay is a big factor, it shouldn’t be the only factor. Also consider—the different types of loan options available, their customer service, closing costs and other fees, etc. This is the largest financial investment you’ll make, so shop around.

That's where we get to help you. It’s usually recommended that homebuyers work with an experienced real estate professional. Not only will they assist you in your search, but they’ll be able to provide advice and support throughout the process—contract negotiations, financing, home inspections, closing, etc. If you choose to not work with an agent, make sure you have an attorney review any contractual or legal documents. We will find you a home and save you in the process.

- Hire a qualified professional to inspect the property—you don't want to cut corners here!

- We have referrals for a reputable inspector, or you can hire your own.

- Review the inspection report with your agent to determine what repairs (if any) you will ask the seller to remedy. Keep in mind, the seller doesn't have to make any repairs, but you can also walk away from the contract if you aren't satisfied with the inspection/resolution.

- Don't ignore any potential issues. Just because you love the home, it doesn't mean you should overlook potential problems.

- Don't ask the seller for more than what's fair. Normal wear and tear should be expected (especially if you are purchasing an older home), so don't assume the seller will replace older (but still working) items.

Let Us Help You Through Entire Process And Save You Too.

|

|

FAQ

|

What ARE THE CLOSING COSTS?

As most homeowners need to get financing, there are closing costs associated with mortgage loan, you will need to pay closing costs, which are fees – charged by lenders and third parties -- related to the purchase of the home. So, in addition to owing the lender the down payment on the home and the principal and interest related to the mortgage, you will also owe the lender and third parties closing costs, which you usually pay at the time that you close on your mortgage. Traditionally, home buyer pays the closing costs, rather than the seller. There are still closing costs such as Title and Escrow fees even if you were to buy a house with cash CAN YOU ITEMIZE THE CLOSING COSTS?

The list below are most closing cost items 1-A fee for credit report. 2-A loan origination fee, which lenders charge for processing the loan paperwork for you. 3-Attorney’s fees, or Escrow Fees 4-Costs involves for any inspection required by the lender or you. 5-Discount points, to buy the interest rate down for lower payment 6-Appraisal fee. 7-Survey fee, which covers the cost of verifying property lines. 8-Title insurance, which protects the lender in case the title isn’t clean. 9-Title search fees, which pay for a background check on the title to make sure there aren't things such as unpaid mortgages or tax liens on the property. 10-Escrow deposit, which may pay for a couple months' property taxes and private mortgage insurance. 11-Pest inspection fee. 12-Recording fee, which is paid to a city or county in exchange for recording the new land records. 13-Underwriting fee. HOW MUCH DOES IT COST?

Usually, home buyers will pay between about 1 and 3 percent of the purchase price of their home in closing costs. So, if your home cost $500,000 you might pay between $5,000 and $15,000 in closing costs. On average, buyers pay roughly $3,700 in closing costs, according to a recent nationwide survey. The reason it is lower than we have listed, Nationwide average home price of $150,000 Lenders are required by law to give you a good faith estimate (GFE) of what the closing costs on your home will be within three days of when you apply for a loan. But these are just an estimate, and many of the fees listed on the GFE can legally change by up to 10 percent, potentially adding thousands of dollars to your final closing cost bill. Within a day of your closing, the lender should give you a HUD-1 settlement statement, which outlines closing costs. Compare this to your GFE and ask the lender to explain what each line item on your closing costs is and why it is needed. Often, many of the fees that make up closing costs are negotiable, and some are completely unnecessary, especially things such as high administrative, mailing or courier costs charged by your lender. If the closing costs come in high, you can walk away from the loan; there are plenty of lenders who might be willing to offer you lower closing costs. How can I avoid closing costs?

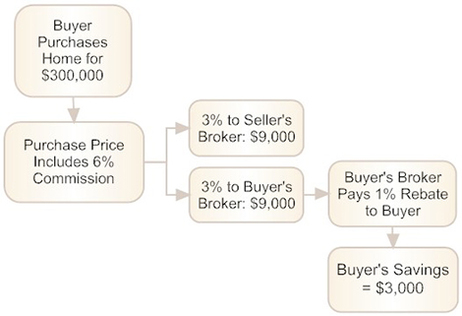

If we represent you, you will receive 1 percent rebate towards your closing costs. So if your home costs $500,000, and assuming your closing costs are $7,500, you will end up paying the closing costs in excess of $5,000, in this example $2,500. Unlike Lender rebate explained below, this does not cost you at all... Lender rebate is another way of eliminate closings costs. It may be called no-closing cost mortgage. Lender rebate costs you higher interest rates than market rate which increases your monthly mortgage payments. It is part of the financing. is homebuyer rebate legal?

Forty states, including California, allow buyer brokers to give rebates to their clients, according to the U.S. Department of Justice. Where are you located?

We are located in Berkeley, CA. Our address is 930 Dwight Way Ste 10A Berkeley, CA 94710 what is your service coverage area?

We serve greater San Francisco Bay Area counties including, Contra Costa, Alameda, Sonoma, Solano, San Francisco, San Mateo, and Marin. Call Us to see if we can help you. |

Are you tired of multiple offers? Do you keep putting offers and someone overbids you? Do you have access to the homes that are not listed? Are you discouraged? DON'T... How would you like to be the only one offering on a property before anyone else? I can not only give you rebates but also get you in a home that is not listed on MLS where you don't compete with many other buyers. You need to contact me to find more about it. |